Above

and beyond

Propulsion components

A rocket relies on its propulsion system for thrust at take-off and again in space to change velocity. High nickel and refractory alloys are used to meet these demands and extend component life under these extreme operating environments. Many of the components require welding, forming, forging and casting. Thermal processing will depend on the material, and is applied to achieve the desired post-fabrication properties. Processes include stress relieving, annealing, brazing, solution and ageing. A comprehensive range of fused coatings is also used to isolate the environment preventing oxidation of the underlying material.

For further information about our services go to

www.bodycote.com/services

Within the Aerospace, Defence & Energy (ADE) business, our customers think and operate globally and increasingly expect Bodycote to service them in the same way. Consequently, the ADE business is organised globally. This gives Bodycote a notable advantage as the only thermal processing company with a global footprint and an understanding of operating in all of the world's key manufacturing areas. A number of Bodycote's multinational customers fall within the compass of ADE and Bodycote intends to continue to leverage its unique market position to increase revenues in these market sectors. The business incorporates the Group's activities in hot isostatic pressing and surface technology as well as the relevant heat treatment services, encompassing 60 facilities in total.

Results

Revenues for the ADE business were £243.5m in 2015 compared to £263.0m in 2014, a decrease of 7.4% (8.1% decrease at constant exchange rates). Overall, revenues from the commercial aerospace sector remained solid but there have been significantly varying levels of demand in different OEM supply chains. Some have focused on significant destocking, while others have delivered good growth on the back of new engine series and airframes. Defence demand has been subdued, resulting in further modest declines in revenue. Demand in the energy sector and particularly the oil & gas sector, has been very weak. Oil & gas revenues have been most depressed in North American heat treatment and in both the USA and the UK for Surface Technology. Declines in HIP PF have been less severe, despite a number of delays to subsea projects, as customers continue to convert to HIP PF from forgings.

Headline operating profit1 for ADE was £59.2m (2014: £70.6m) and headline operating profit margin reduced from 26.8% to 24.3%, demonstrating good cost control in the face of reduced demand.

In 2015, the Group added capacity in a number of facilities, including installation of a new high pressure HIP in the USA. In addition initial works have been undertaken to establish a new aerospace focused facility in South East Poland. In the coming year it is expected that capital expenditure will be slightly above depreciation as further capacity and capability are added to support anticipated growth in the Group's Specialist Technologies and other high-value offerings.

Net capital expenditure in 2015 was £17.4m (2014: £18.4m) which represents 0.9 times depreciation (2014: 0.9 times).

Average capital employed in ADE in 2015 was £234.2m (2014: £236.3m). The Group continues to invest in high-return projects in the ADE business. Return on capital employed in 2015 was 23.0% (2014: 26.6%).

Achievements in 2015

The ADE divisions made further progress during the year in gaining new agreements with a range of customers and for a variety of end uses. In ADE Heat Treatment, new agreements were signed with key suppliers to the growing A350 and A320NEO aerospace programmes. In Surface Technology, a new agreement was signed for the provision of thermal spray coating services for helicopter turbine blades.

The HIP division continues to make good progress, with new customers choosing to use the Group's proprietary Product Fabrication (PF) technology for the first time.

Organisation and people

Total full-time equivalent headcount at 31 December 2015 was 1,785 (2014: 1,898), a decrease of 6.0% compared to the revenue decline in ADE of 8.1% (at constant currencies).

Looking ahead

Order books for commercial aerospace OEMs remain strong, and destocking at certain OEMs and their supply chains is expected to be completed at some point in 2016. We anticipate no near term improvement in the oil & gas sector. Defence markets are expected to be stable. Bodycote believes it will continue to capitalise on its world leading position in the aerospace, defence and energy markets.

- Headline operating profit is reconciled to operating profit in note 2 to the financial statements. Bodycote plants do not exclusively supply services to customers of a given market sector (see note 2 to the financial statements).

ADE revenue by geography

£m

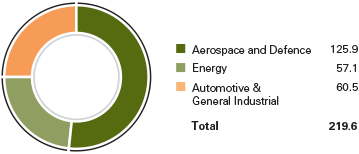

ADE revenue by market sector

£m