Our application of materiality | The description of risks above should be read in conjunction with the significant issues considered by the Audit Committee. These matters were addressed in the context of our audit of the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters. We define materiality as the magnitude of misstatement in the financial statements that makes it probable that the economic decisions of a reasonably knowledgeable person would be changed or influenced. We use materiality both in planning the scope of our audit work and in evaluating the results of our work. We determined materiality for the Group to be £4.8m (2014: £4.9m), which is below 5% of adjusted pre-tax profit, which has been determined to be the most stable basis of underlying performance (2014: 5% of pre-tax profit), and below 1% (2014: 1%) of equity. The adjustment to pre-tax profit relates to the adding back of exceptional restructuring costs of £20.0m in order to use an underlying pre-tax profit base for materiality. There were no such exceptional costs in 2014. We agreed with the Audit Committee that we would report to the Committee all audit differences in excess of £0.15m (2014: £0.145m), as well as differences below that threshold that, in our view, warranted reporting on qualitative grounds. We also report to the Audit Committee on disclosure matters that we identified when assessing the overall presentation of the financial statements. |

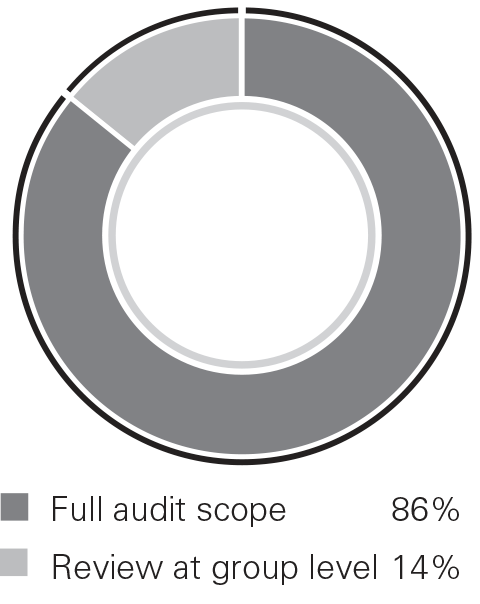

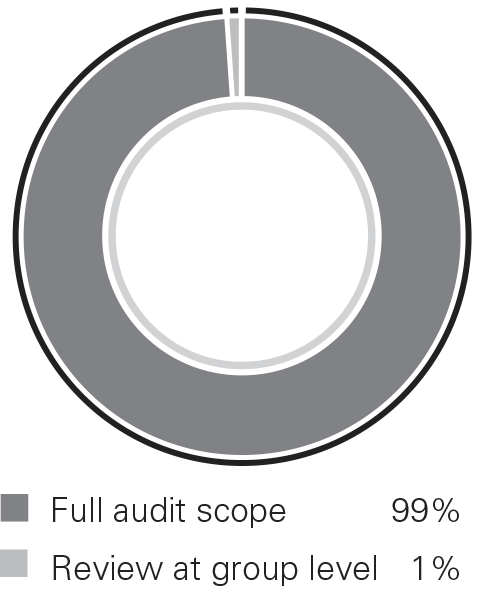

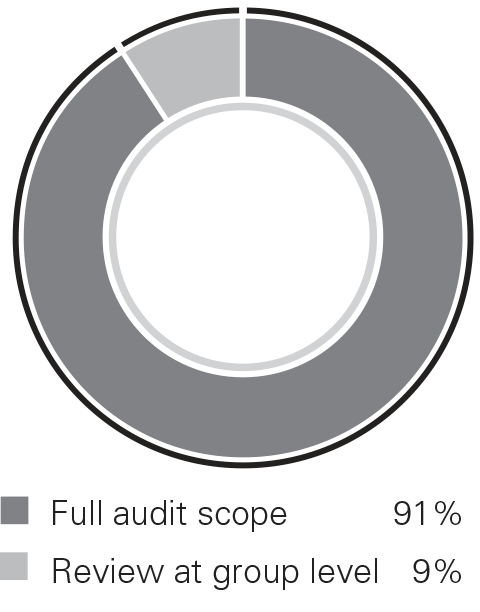

An overview of the scope of our audit | Our Group audit was scoped by obtaining an understanding of the Group and its environment, including group-wide controls, and assessing the risks of material misstatement at the Group level. Based on this assessment, we focused our Group audit scope primarily on the audit work at thirteen countries, being USA, UK, France, Italy, Germany, Poland, Sweden, Netherlands, Czech Republic, Turkey, Singapore, China and Mexico. Consistent with the prior year and as agreed with the Audit Committee, the smaller components in territories such as China, Singapore and Mexico have remained in scope and we have maintained the scoping levels in territories such as Netherlands, Luxembourg, Germany and Turkey. In 2015 we have continued to have direct Group oversight, leadership and control over the components of the Group accounted for in the US Shared Service Centre ('SSC') and in conjunction with our Czech component audit team we jointly audited the components of the Group accounted for at the Prague SSC. As a consequence of the audit scope determined, we achieved coverage of approximately 86% (2014: 86%) of revenue, 99% (2014: 97%) of profit before tax and 91% (2014: 88%) of net assets. Our audit work at each location was executed at levels of materiality applicable to each individual entity which was lower than Group materiality. Component materiality ranged from £0.5m to £2.5m (2014: £0.5m to £2.9m). The Group audit team continued to follow a program of planned visits that has been designed so that a senior member of the Group audit team visits each of the locations included as full scope for the Group audit at least once every three years and the most significant of them at least once a year. In years when we do not visit a significant component we include the component audit team in our team briefing, discuss their risk assessment, attend close meetings by conference call and review documentation of the findings from their work. At the parent entity level we also tested the consolidation process and carried out analytical procedures to confirm our conclusion that there were no significant risks of material misstatement of the aggregated financial information of the remaining components not subject to audit or audit of specified account balances. |

Revenue Profit before tax Net assets |

Opinion on other matters prescribed by the Companies Act 2006 | In our opinion:

- the part of the Board report on remuneration to be audited has been properly prepared in accordance with the Companies Act 2006; and

- the information given in the Strategic Report and the Directors' Report for the financial year for which the financial statements are prepared is consistent with the financial statements.

|

Matters on which we are required to report by exception |

Adequacy of explanations received and accounting records | Under the Companies Act 2006 we are required to report to you if, in our opinion:

- we have not received all the information and explanations we require for our audit; or

- adequate accounting records have not been kept by the Parent Company, or returns adequate for our audit have not been received from branches not visited by us; or

- the Parent Company financial statements are not in agreement with the accounting records and returns.

We have nothing to report in respect of these matters. |

Directors' remuneration | Under the Companies Act 2006 we are also required to report if in our opinion certain disclosures of directors' remuneration have not been made or the part of the Board report on remuneration to be audited is not in agreement with the accounting records and returns. We have nothing to report arising from these matters. |

Corporate Governance Statement | Under the Listing Rules we are also required to review part of the Corporate Governance Statement relating to the Company's compliance with certain provisions of the UK Corporate Governance Code. We have nothing to report arising from our review. |

Our duty to read other information in the Annual Report | Under International Standards on Auditing (UK and Ireland), we are required to report to you if, in our opinion, information in the annual report is:

- materially inconsistent with the information in the audited financial statements; or

- apparently materially incorrect based on, or materially inconsistent with, our knowledge of the Group acquired in the course of performing our audit; or

- otherwise misleading.

In particular, we are required to consider whether we have identified any inconsistencies between our knowledge acquired during the audit and the directors' statement that they consider the annual report is fair, balanced and understandable and whether the annual report appropriately discloses those matters that we communicated to the audit committee which we consider should have been disclosed. We confirm that we have not identified any such inconsistencies or misleading statements. |

Respective responsibilities of directors and auditor | As explained more fully in the Directors' Responsibilities Statement, the directors are responsible for the preparation of the financial statements and for being satisfied that they give a true and fair view. Our responsibility is to audit and express an opinion on the financial statements in accordance with applicable law and International Standards on Auditing (UK and Ireland). We also comply with International Standard on Quality Control 1 (UK and Ireland). Our audit methodology and tools aim to ensure that our quality control procedures are effective, understood and applied. Our quality controls and systems include our dedicated professional standards review team and independent partner reviews. This report is made solely to the Company's members, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the Company's members those matters we are required to state to them in an auditor's report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Company and the Company's members as a body, for our audit work, for this report, or for the opinions we have formed. |

Scope of the audit of the financial statements | An audit involves obtaining evidence about the amounts and disclosures in the financial statements sufficient to give reasonable assurance that the financial statements are free from material misstatement, whether caused by fraud or error. This includes an assessment of: whether the accounting policies are appropriate to the Group's and the Parent Company's circumstances and have been consistently applied and adequately disclosed; the reasonableness of significant accounting estimates made by the directors; and the overall presentation of the financial statements. In addition, we read all the financial and non-financial information in the annual report to identify material inconsistencies with the audited financial statements and to identify any information that is apparently materially incorrect based on, or materially inconsistent with, the knowledge acquired by us in the course of performing the audit. If we become aware of any apparent material misstatements or inconsistencies we consider the implications for our report. |